- Home

- Propositions

- Candidates

- Quick Reference Guide

- Voter Information

- Political Parties

- Audio/Large Print

California Statewide Direct Primary Election June 5, 2018

Official Voter Information Guide

OVERVIEW OF STATE BOND DEBT

PREPARED BY THE LEGISLATIVE ANALYST

This section describes the state’s bond debt. It also discusses how Proposition 68—the $4.1 billion natural resources bond proposal—would affect state bond costs.

Background

What Are Bonds? Bonds are a way that governments and companies borrow money. The state government uses bonds primarily to pay for the planning, construction, and renovation of infrastructure projects such as bridges, dams, prisons, parks, schools, and office buildings. The state sells bonds to investors to receive “up‑front” funding for these projects and then repays the investors, with interest, over a period of time.

Why Are Bonds Used? A main reason for issuing bonds is that infrastructure typically provides services over many years. Thus, it is reasonable for people, both currently and in the future, to help pay for the projects. Additionally, the large costs of these projects can be difficult to pay for all at once.

What Are the Main Types of Bonds? Two main types of bonds used by the state to fund infrastructure are general obligation bonds (which must be approved by voters) and lease revenue bonds (which do not have to be approved by voters). Most of the state’s general obligation and lease revenue bonds are repaid from the General Fund. The General Fund is the state’s main operating account, which it uses to pay for education, prisons, health care, and other services. The General Fund is supported primarily by income and sales tax revenues.

What Are the Costs of Bond Financing? After selling bonds, the state makes annual payments over the next few decades until the bonds are paid off. (This is very similar to the way a family pays off a mortgage.) The annual cost of repaying bonds depends primarily on the interest rate and the time period over which the bonds have to be repaid. Assuming an interest rate of 5 percent, for each $1 borrowed, the state would pay close to $2 over a typical repayment period. Of that $2 amount, $1 would go toward repaying the amount borrowed (the principal) and close to $1 for interest. There likely will be significant inflation over the period during which the state repays these bonds. This means that the dollars used to repay these bonds in the future will be worth less than they are today. Accordingly, after accounting for inflation, the cost of repaying these bonds is lower—roughly $1.50 for each $1 borrowed.

Infrastructure Bonds and the State Budget

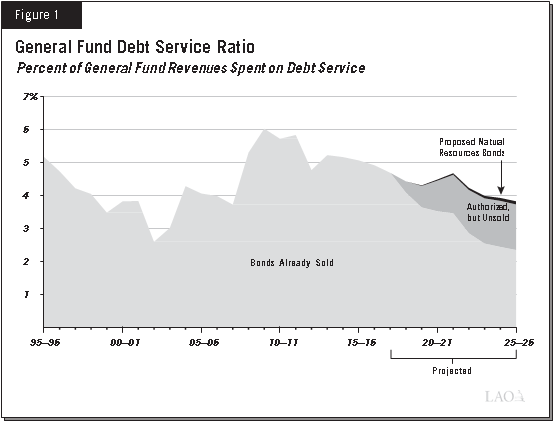

Amount of General Fund Debt. The state has about $83 billion of General Fund‑supported infrastructure bonds on which it is making principal and interest payments. In addition, the voters and the Legislature have approved about $36 billion of General Fund‑supported bonds that have not yet been sold. Most of these bonds are expected to be sold in the coming years as additional projects need funding. In 2017–18, the General Fund’s infrastructure bond repayments totaled close to $6 billion.

This Election's Impact on Debt Payments. The natural resources bond proposal on this ballot (Proposition 68) would allow the state to borrow an additional $4 billion by selling general obligation bonds to investors. The amount needed to pay the principal and interest on these bonds, also known as the debt service, would depend on the specific details of the bond sales. We assume an interest rate of 5 percent and that the bonds would be issued over a ten-year period. We further assume that the last bonds would be repaid 30 years after the final bonds are issued. Based on these assumptions, the estimated average annual General Fund cost would be about $200 million over the next 40 years. This is about 3 percent more than the state currently spends from the General Fund for debt service. We estimate that the measure would require total debt service payments of about $7.8 billion over the 40‑year period during which the bonds would be paid off.

This Election's Impact on the Share of State Revenues Used to Repay Debt. One indicator of the state’s debt situation is the portion of the state’s annual General Fund revenues that must be set aside for debt service payments on infrastructure bonds. This is known as the state’s debt service ratio (DSR). Because these revenues must be used to repay debt, they are not available to spend on other state programs, such as operating colleges or paying for health care. As shown in Figure 1, the DSR is now somewhat below 5 percent of annual General Fund revenues. If voters do not approve the proposed natural resources bond on this ballot, we project that the state’s DSR on already authorized bonds will likely remain somewhat below 5 percent over the next several years and then decrease thereafter. If voters approve the proposed natural resources bond on this ballot, we project it would increase the DSR by less than one-fifth of a percentage point compared to what it would otherwise have been. The state’s future DSR would be higher than shown in the figure if the state and voters approve additional bonds in the future.